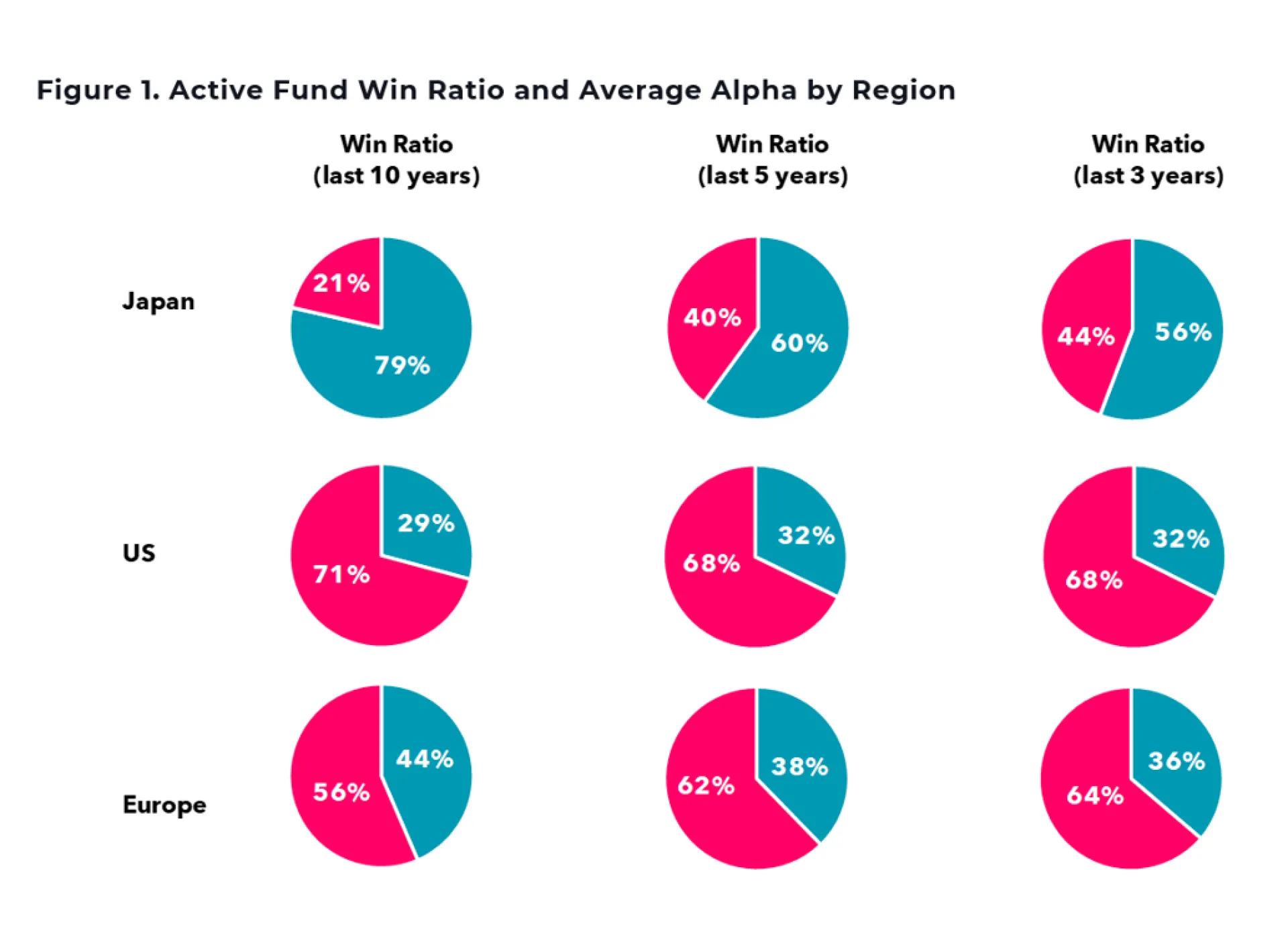

Figure 1 illustrates the win ratio of active funds outperforming their respective benchmarks across Japan, the United States, and Europe over multiple time horizons (3, 5, and 10 years). Across all periods shown, Japanese equity active funds exhibit the highest win ratios among the three regions. Furthermore, the Average Alpha for the same period and market is also shown, indicating it is higher than that of the US and Europe. This persistent pattern highlights Japan as one of the most fertile markets globally for active stock selection.

II. Structural and Cyclical Factors Supporting Active Outperformance in Japan

The superior performance potential of active strategies in Japan is underpinned by several structural and cyclical factors unique to the market.

1. A Large Universe with Limited Analyst Coverage

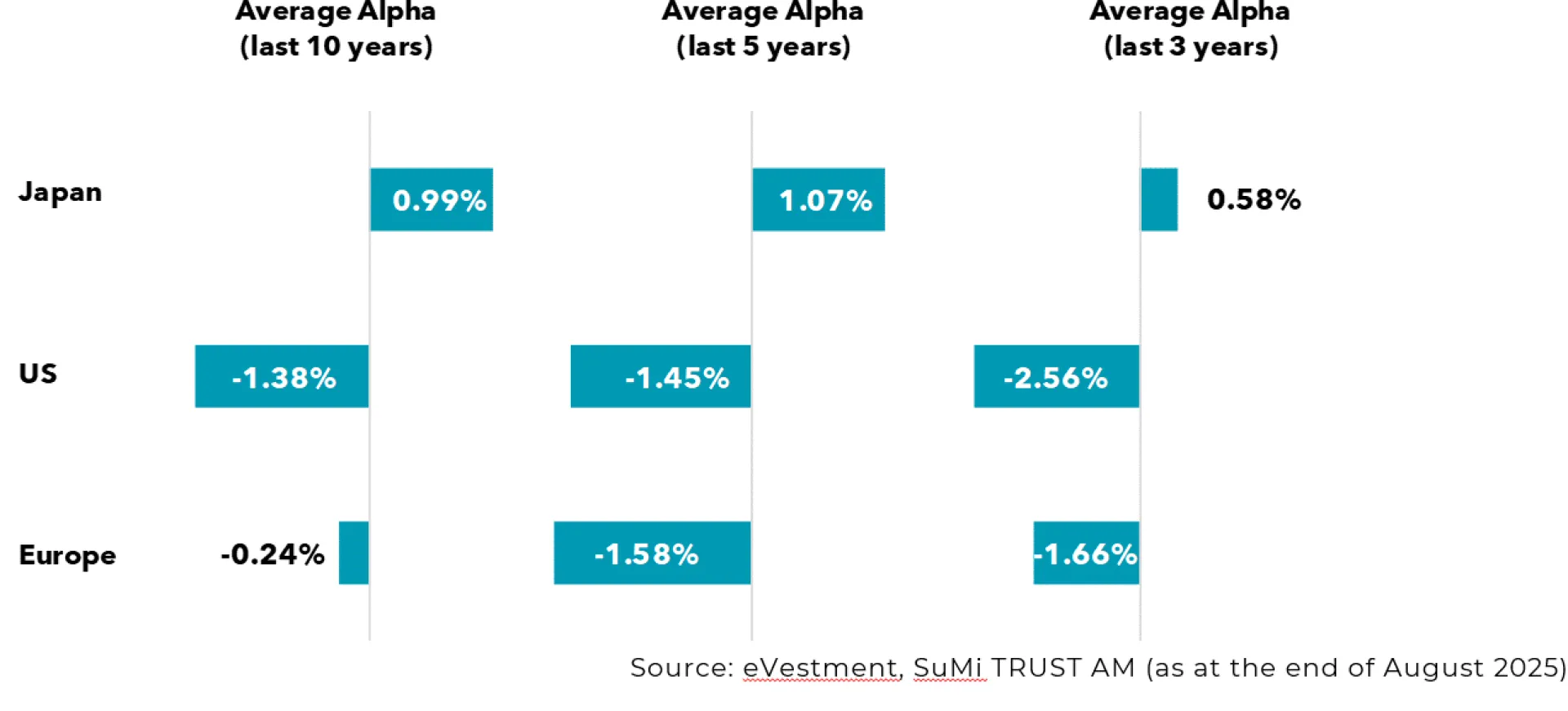

Japan’s equity market is notable for the sheer number of listed companies. Japan has just under 4,000 listed equities, comparable in scale to the listings of Nasdaq and the NYSE. In contrast, the UK has fewer than 1,000 listed companies, while Switzerland has slightly more than 200. This reflects the fact that many small- and mid-sized companies that remain private in other markets are publicly listed in Japan. However, despite the large opportunity set, analyst coverage per stock in Japan remains remarkably low.

While the average analyst coverage is approximately 8.3 analysts per stock in the US, 4.1 in the UK, and 6.6 in Switzerland, Japan averages only around 1.7 analysts per company overall. Even for Japan’s larger companies (TOPIX 500) analyst coverage only averages 9.7 per stock.

To enable a more comparable assessment, Figure 2 focuses exclusively on major large-cap indices: the S&P 500 (US), TOPIX 500 (Japan), FTSE 350 (UK), Swiss Market Index (Switzerland), and GDAX Index (Germany).

Even when limiting the analysis to large-cap universes, analyst coverage in Japan remains significantly lower than in other developed markets. In such an environment, active managers with strong local research teams and direct corporate access are better positioned to uncover alpha opportunities that cannot be identified through publicly available financial data alone. Deep fundamental research and ongoing dialogue with management become critical sources of competitive advantage.

2. Japan at a Historic Economic Turning Point

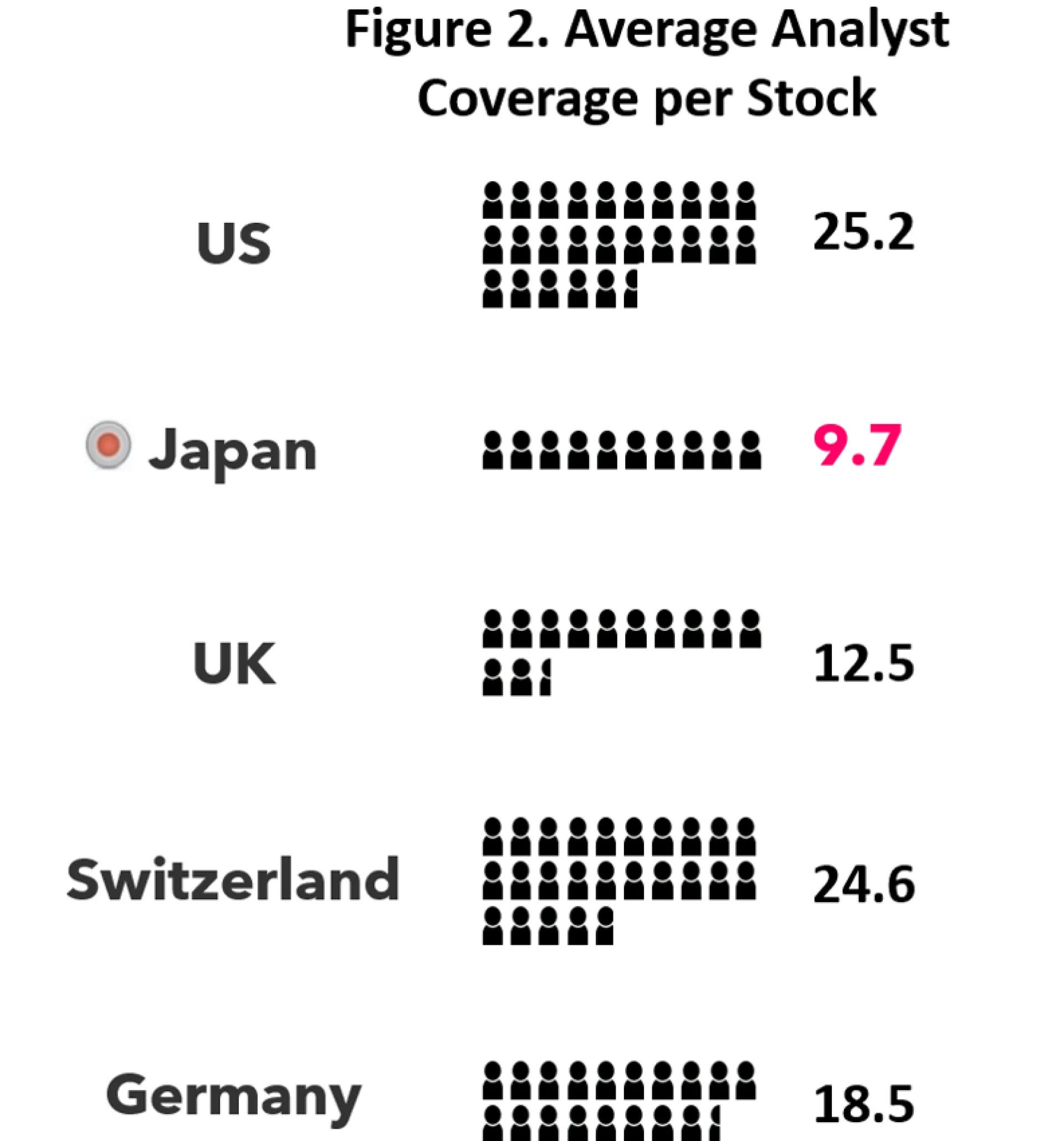

Japan is undergoing a profound macroeconomic transition after nearly three decades of deflation. The economy is shifting toward a more stable inflationary environment, accompanied by rising interest rates.

As shown in Figure 3, Japan moved away from its long-standing negative interest rate policy in 2024 and has entered a rate-hiking cycle. Unlike many developed economies that have struggled with sharp inflation spikes in recent years, Japan’s inflation has emerged gradually and remains relatively moderate. Importantly, wage growth has also continued, reinforcing the credibility of Japan’s exit from deflation.

In recent years, there might be a view that, rather than investing considerable time and effort in seeking out active management worthy of investment to capture major shifts in the Japanese economy such as escaping deflation, it has been more advantageous to swiftly capture the rise in Japanese equities through vehicles like ETFs.

We continue to believe Japanese equities will rise steadily, but we view the phase of sharp increases driven by corrections to extreme undervaluation as having concluded. We now see the market entering a phase of appreciation aligned with the underlying reality of the economy and corporate earnings. In such a phase, a bottom-up approach focusing on individual company performance proves more effective than a top-down approach centred on macroeconomic factors.

Looking ahead to future changes in the Japanese economy, we believe that individual stock selection will carry even greater weight when investing in Japanese equities. Let us consider how the changes in the Japanese economy compared to pre-pandemic times will impact corporate earnings.

While we anticipate that overall earnings for Japanese companies will see double-digit growth both this fiscal year and next, we believe that performance will increasingly polarise in response to these economic shifts.

Specifically, companies will divide into those capable of growing sales and profits by adapting to the structural changes in the Japanese economy, and those lagging behind due to outdated corporate structures. Wages, which had been slow to rise, have clearly begun increasing, marking an escape from years of deflation. In an inflationary economy, companies must pass on rising costs to prices. Customers may accept price increases for superior products or services, but this proves difficult for mass-produced, run-of-the-mill goods. Whereas previously everyone maintained prices at the same level, henceforth differences in the ability to pass on costs will create disparities.

The Bank of Japan has implemented interest rate hikes, returning Japan to a world of interest rates. Amidst an abundance of capital, any company could easily borrow money.

Going forward, only companies with sound financial health and growth potential will be able to secure longer-term funding at lower interest rates. Differences will emerge in the ability to execute investments aimed at increased production or quality improvement.

Japan faces a significant labour shortage, particularly among younger workers. Many shops and businesses struggle to recruit staff, sometimes curtailing sales or production due to understaffing. Conversely, promising companies attract talented individuals. Differences in recruitment capability will manifest as disparities in corporate strength.

Differences in performance and corporate strength, influenced by economic shifts, will manifest as disparities in future share price performance. Amidst anticipated corporate polarisation, investing in the surviving companies becomes crucial. Unlike passive management, which invests across the entire market, active management involves selective investment in individual stocks. Considering the recent changes in the Japanese economy, the significance of active management – selectively investing in the surviving companies – has increased further.

III. Governance Practices can Translate Directly into Superior Investment Outcomes

3. Accelerating Divergence from Corporate Governance Reform

Corporate governance reform, led by the Japan Exchange Group (JPX), is another powerful driver of dispersion in Japanese equities. The gap between companies that proactively address governance requirements and those that do not has widened materially.

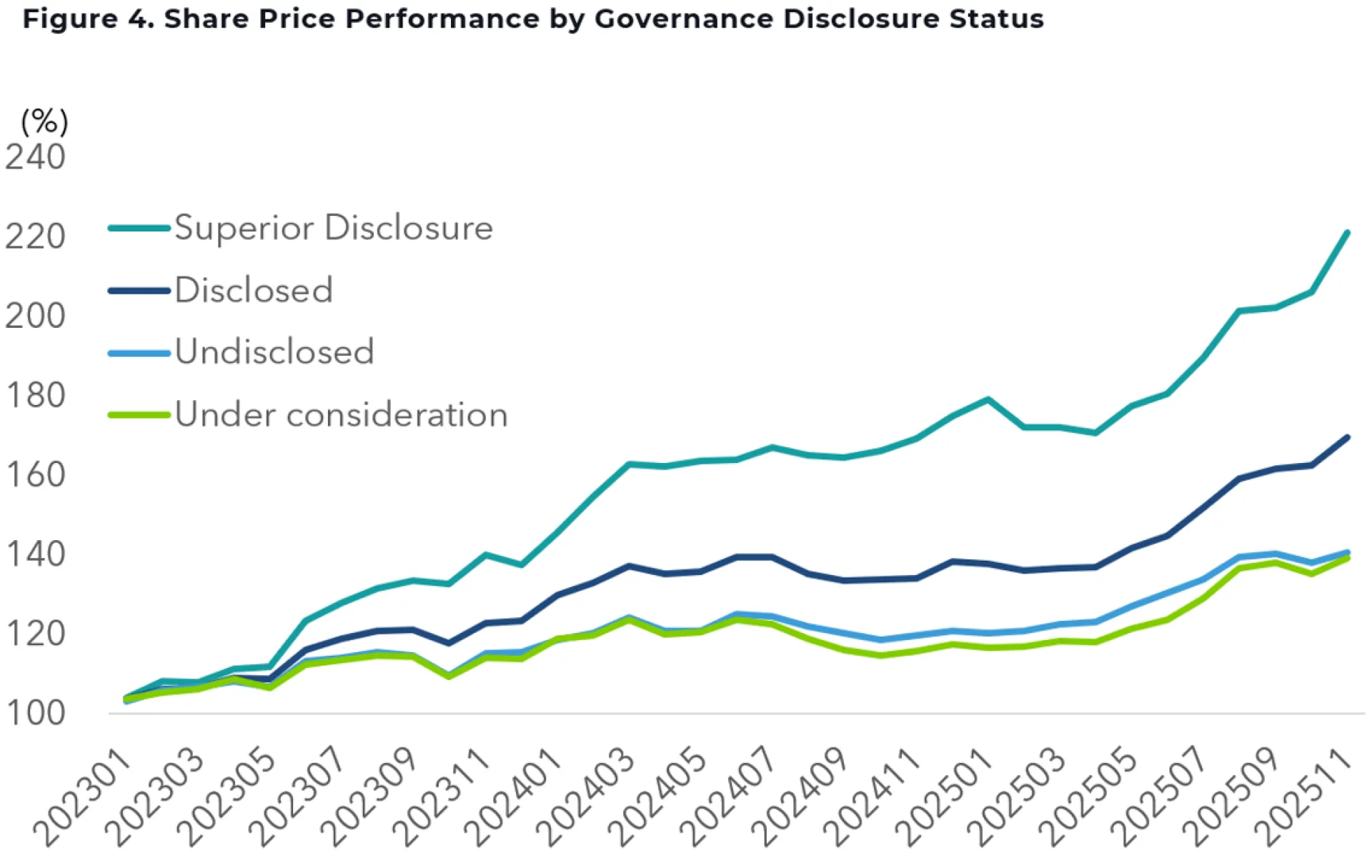

Note: These figures represent the weighted average of the constituent stocks at each disclosure level as of November 2025. Calculated with a base of 100 at the end of December 2022.

‘Superior Disclosure’ refers to companies featured in the case studies published by the Tokyo Stock Exchange on 21 November 2024 as companies promoting initiatives that incorporate investor perspectives.

Source: Japan Exchange Group, SuMi TRUST AM (as at the end of November 2025)

Based on JPX disclosure data, Figure 4 compares share price performance by governance disclosure status, rebased to 100 at the end of December 2022 and measured through the end of November 2025. Companies that actively disclose concrete initiatives to improve governance have significantly outperformed those that do not.

This evidence reinforces the importance of selective evaluation and active engagement. It also illustrates how the effective use of non-financial information such as governance practices can translate directly into superior investment outcomes in the Japanese equity market.

IV. Local Manager, Local Knowledge

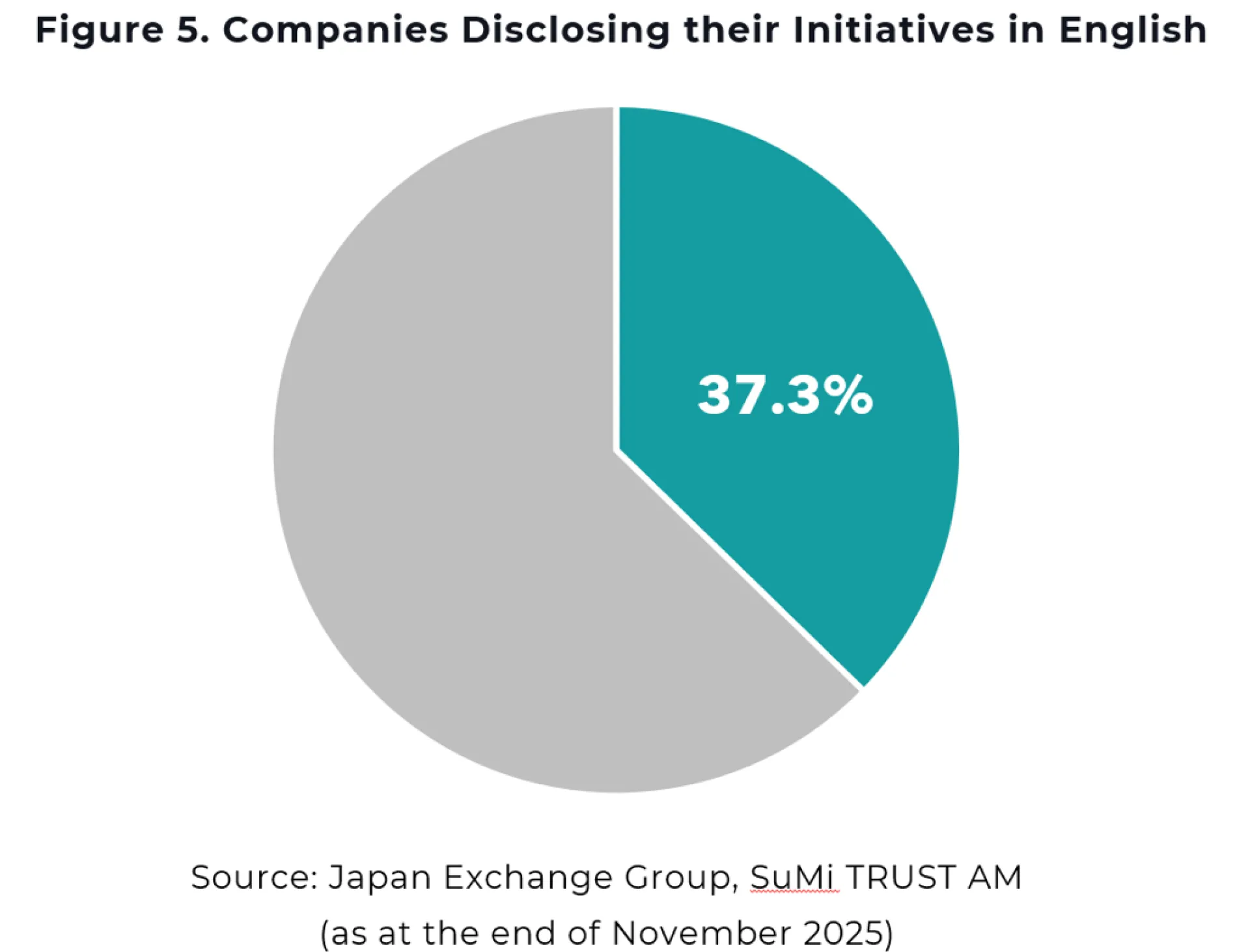

The advantage of local asset management firms with analyst teams who are native Japanese speakers is considerable even in the effective use of non-financial information. Among TOPIX constituent companies, 1,503 firms — representing 70% of the total — disclose initiatives aimed at management practices conscious of capital costs and share prices. However, only 806 companies — 37% of the total — disclose these initiatives in English (Figure 5). This current situation can be considered an advantageous environment for Japanese native speakers.

V. Conclusion

Taken together, these structural inefficiencies, macroeconomic regime changes, and accelerating governance-driven dispersion provide a strong foundation for active management in Japanese equities. For global investors, Japan represents not merely a geographic allocation, but a market where skilled active managers can consistently add value. Selecting high-quality active strategies with deep local expertise is therefore essential when building long-term exposure to Japanese equities.